In recent months, we saw a flurry of widely diverging predictions on the 2017 global PV market demand – 85 GW from GTM, 79 GW from IHS and Bloomberg, and 74 GW from EnergyTrend – the key differentiating variable being China, the world’s largest market by far with its importance only matched by its opacity.

To understand the Chinese market, it is important to understand that domestic PV demand is to a large extent centrally planned. 2016 was in particular an exciting year for Chinese PV policy: the release of the 13th Five-Year Plan for Energy cut the 2020 PV target from 150 GW to 105 GW, utility-scale FiT rates were slashed by the largest margin in history, and the so-called “Top Runner” program grew to 5.5 GW in size from 1 GW the year before. Phase 1 of a new “PV for Poverty Alleviation” program was introduced, also a sizable 5.2 GW.

It also goes without saying that with China being by far the largest global market and the home turf of the world’s largest PV companies, domestic developments have a far-reaching impact on the global PV landscape, whether intentionally or inadvertently. In this article, Apricum presents a deep dive into the policies that have taken shape over the past two years, and highlights how these can explain the 2016 H2 global price depression, the surge in high-efficiency cell technology investments, as well as how the policies can inform our short- and mid-term market forecast.

Key Programs Driving Chinese PV Market Demand

PV installation volumes in the Chinese market are largely centrally planned. Prior to 2015, PV demand was driven almost solely by utility-scale projects under the FiT program, whereas since 2015 the market has become more diversified, with distributed PV, the Top Runner Program, and the PV for Poverty Alleviation program taking up significant market share.

Figure 1 – China’s major national PV programs

| National PV programs | Description | |

| 1 | Standard FiT “Build Plan”:

|

|

| 2 | Top Runner Program |

|

| 3 | Poverty Alleviation Program |

|

1. Utility-Scale PV FiT and the Build Plan

The FiT program has been the bedrock of the Chinese PV market historically. There are three key series of policy documents that shape China’s FiT program: the “PV Build Plan”, released annually, which sets project quotas by province; the FiT rate change notices, which publishes the FiT rate for the budget year; and the “Renewable Energy Subsidy Catalog” that greenlights projects to begin receiving FiT disbursements.

Build Plan

Early each year, the NEA publishes a “Build Plan” that stipulates the approved capacity quota for the year by province. Only projects accepted under the Build Plan are eligible to receive FiT under the year’s national Renewable Energy Subsidy budget: projects registered under the 2015 Build Plan, for example, receive 2015 FiT rates. The commissioning deadline for utility-scale projects is typically June 30 of the next year, locally known as the “630” deadline, and does not necessarily follow the calendar year. The spectacular 22.5 GW installed in the first half of 2016, including the 11 GW installed in June 2016, was to a large extent the result of this timeline structure: whereas 23.1 GW was planned for under the 2015 Build Plan, only 13.7 GW were built in calendar year 2015, and the remaining projects spilled over into 1H 2016.

Many provinces use a first-come-first-served methodology in administering the Build Plan, whereby projects secure their place in the Build Plan based on the order of their completion. In many provinces, this has historically resulted in an unregulated rush to finish first, resulting in an excess of projects that are unable to secure FiT. In these cases, projects that complete after the year’s Build Plan has been fully allocated are backlogged for consideration in the next year’s Build Plan, and in the meantime receive only wholesale tariff for their electricity production.

Table 1 – PV Build Plan vs. Actual Build 2014–2016 [GW]

| Annual Build Plan | 2014 | 2015 | 2016 | |

| Utility-scale | Plan | 6.1 | 23.1 | 12.6 |

| Actual | 8.6 | 13.7 | 30.3 | |

| Over (under) build | 2.5 | (9.4) | 16.7 | |

| Distributed | Plan | 8.0 | n/a | n/a |

| Actual | 2.1 | 1.4 | 4.2 | |

| Over (under) build | 5.9 | n/a | n/a | |

Source: NEA

In recent years, these excess projects are so numerous that the NEA towards the end of the year is eventually pressured into expanding the original Build Plan to accommodate them:

In 2014, the initial Build Plan called for 4 GW of utility-scale and 8 GW of distributed PV; while the utility-scale target was exceeded, the distributed target fell short by far, and the NEA eventually expanded the utility-scale target by 2 GW.

The initial Build Plan for 2015 allocated 17.8 GW to utility-scale PV and removed the quota restriction on the distributed segment; utility-scale target was later further increased to 23.1 GW.

In 2016, the initial Build Plan called for only 12.6 GW of utility-scale plants, but with a large number of projects in backlog and under construction/development, the NEA in December 2016 allowed provinces to apply to “borrow” quota from their 2017 allocation, for up to 1 GW, with the caveat that provinces applying for more than 500 MW would not receive any quota at all under the 2017 Build Plan, and that any new allocations made must be selected in a price-based competitive tender, under which pricing has to form at least 30% of the evaluation framework. Applications for a total of 11.7 GW were filed; of these, eight provinces applied for the full 1 GW. Results of the application are not yet released, although several provinces have already independently announced the approval of their applications.

Despite being already far into the year, the 2017 Build Plan has also not yet been released as of May 2017.

FiT rate change notices

National FiT rates are released separately from the Build Plan in FiT rate change notices by the National Development and Reform Commission (NDRC); these notices typically also stipulate the commissioning deadline for projects to receive the year’s rates. While there is no mandatory annual step-down, the intention under the 13th Five-Year Plan is to move towards a competitive tendering model, reaching grid parity for distributed PV by 2020.

Table 2 shows the development of FiT rates over the years. Notice there was no FiT step down in 2015. This, together with the decline in component prices, created a strong profit margin for developers that contributed to the 2015 Build Plan demand and hence the 2016 H1 installation peak.

Table 2 – China national PV FiT rate over the years [RMB/kWh]

| Resource region | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 |

| I | 1.15 | 1.00 | 1.00 | 0.90 | 0.90 | 0.80 | 0.65 |

| II | 0.95 | 0.95 | 0.88 | 0.75 | |||

| III | 1.00 | 1.00 | 0.98 | 0.85 | |||

| Distributed PV | 0.42 | 0.42 | 0.42 | 0.42 |

Source: NDRC and NEA

Note: (*) Regional solar resource in China is classified as class I, II or III, in descending order of abundance; see Table 5 for the designation by province.

Renewable Energy Subsidy Catalog

Even after successful registration and construction completion under the respective Build Plans, securing the FiT rates, developers must wait upon their project being included in the oft-delayed Renewable Energy Subsidy Catalog, in part confirming that their completed plant fulfils all FiT criteria, before they can begin receiving FiT disbursements. Plants operating in the meantime receive only the wholesale electricity tariff.

Due to a combination of insufficient funding for the Renewable Energy Fund, which funds the national FiT, and runaway market growth in the years of 2013–2016, a crippling subsidy payment backlog for FiT projects has developed. Industry sources estimate that this backlog amounts to USD 870M at end 2016. From a chronological perspective, an Apricum source estimates that the sixth and latest release of the Catalog (in August 2016) at best included projects completed through mid 2015, and so none of the projects completed in the last two years (mid 2015 through mid 2017) have yet seen a single cent.

Distributed PV FiT

In 2015, the Build Plan was amended to remove the cap on distributed PV; local authorities are required to process distributed PV submissions for Build Plan registration promptly and with priority. In the latest release of the Renewable Energy Subsidy Catalog in August 2016, rules were further amended such that distributed PV systems could begin receiving FiT disbursements immediately upon Build Plan registration, instead of waiting for Catalog confirmation.

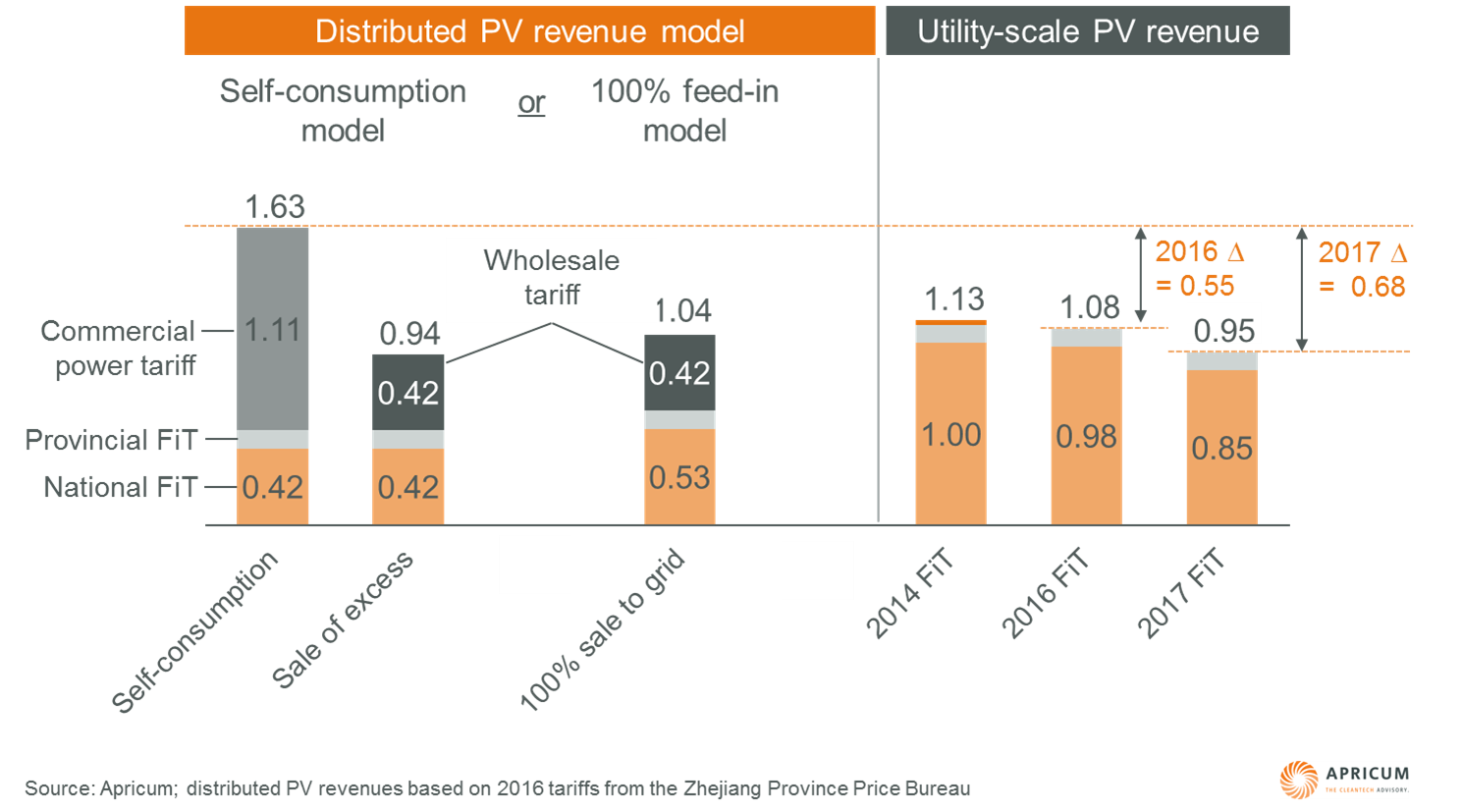

The national FiT rate for distributed PV has stayed constant at RMB 0.42/kWh over the last four years, in contrast to the declining utility-scale national FiT rate. An owner of a distributed PV system in China has two choices of tariffs: 1) self-consumption with sale excess PV generation to the grid, and 2) sale of all PV generation to the grid. In Zhejiang province, for example, the province with the highest amount of distributed PV installed (cumulatively 2.1 GW as of Dec 16), a commercial system installed would earn the following revenue streams under the respective models:

Figure 2 – Zhejiang province distributed vs. utility-scale PV installation revenues

Distributed PV – Self-consumption model:

For the consumed portion:

1.11 C&I power tariff (savings)1 + 0.42 national FiT + 0.10 provincial FiT = 1.63 RMB/kWh

For the fed-in portion:

0.42 wholesale tariff + 0.42 national FiT + 0.10 provincial FiT = 0.94 RMB/kWh

Assuming 80% is self-consumed and 20% is fed into the grid, the average revenue is 1.49 RMB/kWh.

Distributed PV – 100% feed-in model:

0.42 wholesale tariff + 0.53 national FiT + 0.10 provincial FiT = 1.04 RMB/kWh

[1] Based on peak power price for a Zhejiang commercial entity using <1000V, which applies for most of the regular working day from 08.00–11.00 and 13.00–19.00

The 100% feed-in model thus benefits from a higher national FiT, but is not exposed to any potential savings from future electricity price increases. Its continued attractiveness also depends more heavily on the national FiT staying high relative to the self-consumption model.

It is also key to note that distributed PV in China is defined as installations under 20 MW with a 35kV connection, under 6 MW with a 10kV connection, and under 500kW with a 400V connection. Given that a 20 MW plant is essentially a utility-scale plant, we see strong likelihood that developers will continue driving demand and reaping FiT benefits via the distributed channel.

2. PV Top Runner Program

Relatively new to China’s PV landscape is the PV Top Runner Program, which was introduced in 2015 to give Chinese PV players economic incentives to invest in new and innovative technologies. There are two parts to the Top Runner Program: 1) a policy component where the NEA sets the minimum performance parameters for PV cells, modules and inverters eligible to be a Top Runner component, and 2) a project component where the NEA organizes tenders that utilize exclusively Top Runner components.

The pilot round launched in 2015 consisted of one 1 GW tender of multiple projects in Shandong province, completed by end-June 2016. The second round launched in 2016 expanded to eight tenders (also called “bases”) in five provinces, totaling 5.5 GW. All of the equipment used in these projects need to meet minimum requirements of 16.5%/17.0% efficiency for multi-crystalline and monocrystalline silicon modules respectively. A supply crunch resulted, particularly on the multi-crystalline front, as monocrystalline modules of the time could more easily meet the 17.0% efficiency requirement than multi-modules the 16.5% requirement. This prompted the 2015–2016 rush towards PERC and monocrystalline silicon capacity expansion, in anticipation of next year’s tenders and more stringent requirements to come.

Table 3 – Standard vs. Top Runner Program minimum module performance requirements

| Regular | Top Runner | |||||

| No. cells | Multi | Mono | Multi | Mono | ||

| Efficiency | – | 15.5% | 16.0% | 16.5% | 17.0% | |

| Power (equivalent) |

60 | 255 W | 260 W | 270 W | 275 W | |

| 72 | 305 W | 315 W | 325 W | 330 W | ||

Source: NEA

In addition to minimum efficiency requirements, the Top Runner Program is structured such that there are special carve-out projects (min. 50 MW) within individual tenders for “new technologies”, which in 2015 was loosely defined to include PERC, IBT, HIT cell technologies. What the program does is provide Chinese players with a sizable, assured end-market for technologies that are commercially available but not yet competitive. It encourages Chinese players to invest in niche, high-efficiency technologies currently only produced by the likes of SunPower and Panasonic.

Round 3 of the program is currently in development. Whereas Round 2 had a mandatory minimum 30% pricing component in the evaluation framework, Round 3 is expected to eliminate that in favor of emphasizing on innovative technological development. An update to the Top Runner minimum performance criteria is also expected.

3. PV for poverty alleviation

The third pillar of PV demand in China in 2017 and onwards will come from the PV for Poverty Alleviation Program, which was introduced by the NEA in March 2016. The program aims to supplement by a minimum of RMB 3,000/year (USD 435) the incomes of 2 million impoverished households across 35,000 villages, specifically targeting people unable to work and the physically impaired. This will be achieved by either the granting of PV systems to individual households or sharing with targeted households a portion of the revenues generated from the designated PV installations.

The first phase of the program released in October 2016 has planned for 2.18 GW of small-scale PV, as well as 2.98 GW of utility-scale plants. Within the small-scale segment, beneficiaries can be single households or villages. Funding is to be sourced from a mix of government grants, state-backed concessionary loans, and private sector investments. The portion of income attributable to the government-funded equity share will be distributed among the beneficiaries.

| Category | Phase 1 size | Benefits to the poor | Source of funding |

| Household-level | 2.18 GW | Households directly own the PV systems and any benefits thereby derived | Local government responsible for fundraising; may access various provincial and national poverty alleviation funds |

| Village-level | Local governments raise funds and invest on behalf of the poor; households receive dividends from “their” equity share of the power plants | ||

| Utility-scale | 2.98 GW | Developers and co-investors; local governments; concessionary loans from the China Development Bank and the Agricultural Development Bank of China |

Source: NEA

While not as globally significant as the FiT or Top Runner Program, the PV for Poverty Alleviation Program represents a significant source of demand alternative to the FiT program.

China PV Market Trends through 2020 (the 13th Five-Year Plan)

Globally, China’s FiT policy structure has historically had the effect of creating seasonal price trends, namely the price surge in H1 and the immediate plummet after the June 30 mark. Beginning in 2017, the implementation of the Top Runner tenders and Poverty Alleviation projects at scale would begin to moderate this seasonality. The remainder of the article will highlight key trends we observe in the Chinese market.

a. Shift Towards Distributed PV

The message from 2016 policies is that the government going forward will be putting overwhelming emphasis on distributed PV in a firm response to the chronic problem of curtailment, which in Class I resource regions like Xinjiang had at some point soared to 50% due to insufficient large-scale transmission capacity to dispatch to demand centers.

In the Renewable Energy and Solar 13th Five-Year Plan released late 2016, the government cut massively the 2020 cumulative PV installation target from 150 GW to 105 GW. This cut, however, takes place almost wholly in the utility-scale target – the new utility-scale target of 45 GW is essentially already far exceeded at the point of release of the plan, and is not meaningful except as an indicator of the shifting winds at the highest regulatory levels. Installed utility-scale PV capacity at end 2016 was 67 GW. Distributed PV, on the other hand, has 50 GW of headroom to fill out over the next four years (see Table 4).

Table 4 – New PV installations targets under the 13th Five-Year Plan [GW]

| Old target for 2020 | New target for 2020 | Installed capacity 2016 | Gap to target | |

| Utility-scale | 80 | 45 | 67.1 | Exceeded |

| Distributed | 70 | 60 | 10.3 | 50 |

| Total | 150 | 105 | 77.4 | 27.6 |

Source: NDRC and NEA

This is, to be certain, not the government’s first effort to promote distributed PV. The 2014 PV Build Plan, for example, was structured as 6.1 GW utility-scale and 8.0 GW distributed – but whereas the utility-scale target was exceeded by 2.5 GW, only 2 GW of distributed PV was built. This was due to the more favorable economics of utility-scale vs distributed solar in 2014, a gap that has narrowed over the years as the national FiT for utility-scale plants tumbled, while the national FiT for distributed PV remained stable at 0.42 RMB/kWh (see Table 2).

Distributed PV now also has the advantage of immediately being able to receive FiT disbursements. With such a large subsidy backlog in place, including the massive 34 GW installed in 2016, utility-scale projects installed today present a much greater cash flow risk to developers than distributed.

Moreover, in many provinces like Jiangxi, Anhui, Henan and Hubei, provincial regulators have already issued public notices advising developers to halt further PV projects, as the project pipeline in development, construction and completed have already exceed any likely FiT Build Plan allocation for the respective provinces through 2020. Developers in such provinces have every incentive to build only distributed PV today.

This shift towards distributed PV was already apparent in Q1 2017, which saw distributed installations soar to 34% of total installations from 14% in Q1 2016, or a 150% year-on-year increase, even as total installations stayed flat at 7.2 GW. Apricum industry sources expect distributed installations to increase in the second half of the year in anticipation of the price decline.

Table 5 – China 2016 full year and 2016/2017 Q1 installations by province

| Province (Region, City) |

Resource region | Full Year 2016 [MW] | 1Q 2017 | 1Q 2016 | ||||

| Utility-scale | Distributed | Total | Distributed [MW] | % of total | Distributed [MW] | % of total | ||

| Total | 30,310 | 4,230 | 34,540 | 2,430 | 34% | 980 | 14% | |

| Beijing | 2 | 30 | 50 | 80 | – | – | – | – |

| Tianjin | 2 | 440 | 30 | 470 | 2 | 100% | 10 | 100% |

| Hebei | 2, 3 | 1,920 | 110 | 2,030 | 180 | 36% | – | – |

| Shanxi | 2, 3 | 1,720 | 110 | 1,830 | 60 | 50% | 30 | 38% |

| Inner Mongolia | 1, 2 | 1,660 | -180* | 1,480 | 10 | 5% | – | – |

| Liaoning | 2 | 290 | 70 | 360 | 10 | 25% | 10 | 50% |

| Jilin | 2 | 450 | 40 | 490 | 50 | 83% | 20 | 67% |

| Heilongjiang | 2 | 110 | 40 | 150 | 5 | 50% | 10 | 20% |

| Shanghai | 3 | – | 140 | 140 | 40 | 100% | 30 | 100% |

| Jiangsu | 3 | 700 | 530 | 1,230 | 300 | 45% | 140 | 78% |

| Zhejiang | 3 | 880 | 870 | 1,750 | 450 | 43% | 220 | 42% |

| Anhui | 3 | 1,780 | 470 | 2,250 | 390 | 36% | 90 | 16% |

| Fujian | 3 | 80 | 40 | 120 | 40 | 25% | – | – |

| Jiangxi | 3 | 1,540 | 310 | 1,850 | 60 | 13% | 20 | 4% |

| Shandong | 3 | 2,470 | 750 | 3,220 | 400 | 87% | 200 | 23% |

| Henan | 3 | 2,340 | 100 | 2,440 | 120 | 12% | 10 | 4% |

| Hubei | 3 | 1,240 | 140 | 1,380 | 70 | 41% | 50 | 16% |

| Hunan | 3 | – | 10 | 10 | 100 | 67%- | – | – |

| Guangdong | 3 | 610 | 310 | 920 | 80 | 42% | 80 | 80% |

| Guangxi | 3 | 40 | 20 | 60 | -3* | -43% | – | – |

| Hainan | 3 | 50 | 50 | 100 | – | – | – | – |

| Chongqing | 3 | – | – | – | 1 | 100% | – | – |

| Sichuan | 2 | 570 | 30 | 600 | 2 | 100% | 20 | 11% |

| Guizhou | 3 | 430 | – | 430 | – | – | – | – |

| Yunnan | 2 | 1,450 | -10* | 1,440 | 10 | 100% | – | – |

| Tibet | 3 | 160 | – | 160 | – | – | – | – |

| Shaanxi | 2, 3 | 2,100 | 70 | 2,170 | 20 | 4% | – | – |

| Gansu | 1, 2 | 740 | 20 | 760 | – | 0% | – | – |

| Qinghai | 1, 2 | 1,180 | 10 | 1,190 | 10 | 13% | – | – |

| Ningxia | 1 | 1,990 | 180 | 2,170 | 10 | 100% | 30 | 8% |

| Xinjiang | 1, 2 | 3,330 | -40* | 3,290 | 20 | 100% | – | – |

Source: NEA

*) Note that the official NEA source publishes only total and utility-scale figures, and distributed PV figures are derived the latter from the former; the source recognizes accounting errors in the prior period that leads to the total installed numbers being less than utility-scale

The shift towards distributed PV has also had the effect of moving the nucleus of PV activity from the sparsely populated Class I resource regions to the more populous eastern provinces, in line with government plans to reduce the burden on transmission capacity. Overall curtailment rate markedly improved from 16.1% in Q1 2016 to 10.7% in Q1 2017.

b. Domestic Margin Squeeze and Internationalization

As FiTs are slashed and phased out and projects adopt competitive, price-based tendering models, margins of PV component manufacturers and developers alike increasingly narrow.

Tenders from the Round 2 Top Runner Program held in 2016 produced record-low bids. The RMB 0.45/kWh (USD 6.5 cents) bid by Yingli for a 100 MW project in Inner Mongolia, for example, was 44% below the prevailing FiT rate and lower than the RMB 0.50/kWh retail electricity rate.

With profits running dry domestically, we see a strong push by many Chinese companies for greater internationalization. With the bankruptcy of SolarWorld and the bulwark of protectionist policies, we foresee even tougher times ahead for small-scale local players in Europe and the USA.

c. Chinese PV Companies to Lead Technology Development

What we see in the Top Runner program is the first concerted effort by Chinese regulators to push Chinese PV companies to technology leadership, away from the comfortable cost leadership and economies-of-scale business model that has been the modus operandi thus far.

By setting the gap between multi- and monocrystalline Top Runner efficiency requirements at a narrow 0.5%, regulators have signaled that they are strongly in favor of mono technologies, and this clear signal has given domestic companies the confidence to pursue capital-intensive expansions.

In the two years since the introduction of the Top Runner program, we have already witnessed PERC production becoming the industry norm where previously it was a fringe upgrade. There has also been a marked increase in investments in monocrystalline wafer and cell capacities, given mono produces better results with the PERC upgrade than multi. LONGi for one has close to doubled its monocrystalline wafer capacity from 4.5 GW to 7.5 GW, and has furthermore entered into a 5 GW joint venture with Trina. In June 2016, Zhonghuan Semiconductor, the second largest domestic mono wafer supplier, launched the construction of a new 6 GW mono polysilicon and wafering facility, and in February 2017 signed a 5 GW P-Series manufacturing joint venture with SunPower. Chinese PV module manufacturers on their websites today may separately showcase a new module category labeled “high-efficiency”, to highlight top-of-the-line modules that fulfill Top Runner Program requirements.

To defend against this encroachment of mono-PERC, GCL, JA Solar and Jinko have begun looking into cell texturing as a potential avenue of enhancing their existing multi production capacities lest they become obsolete. Unless they succeed, we are likely to see to see greater convergence in mono- and multi-crystalline module prices and market share.

The key takeaway here is that the Chinese companies, for both reputational concerns and to serve their largest market, have proven very responsive to technology requirements posed domestically, which in turn gives the Chinese government a strong degree of control over the global rate of PV technology advancement. In the near to medium term, we expect that technologically-differentiated PV companies like SunPower and Panasonic, as well as First Solar and Solar Frontier, will face significant threat on their ability to compete on a price per watt basis.

Conclusion

Taking into consideration the pillars of PV demand introduced above and the recent market trends, we expect 2017 installations to come from the following sources:

- Top Runner Program: 5 GW

- Poverty Alleviation Projects: 2 GW; not all may be installed in 2017 as yet no deadlines have been announced

- Utility-scale FiT 1H: Taking into account the excessive building pattern in 2016 and the 4.8 GW built in Q1, 13–15 GW is likely

- Utility-scale FiT 2H: The 2017 Build Plan has not yet been released, but as many as eight provinces will not receive new allocations due to their overdraft under the 2016 Build Plan; we believe installations will be lower than the ~10 GW in 2H last year, at 5–7 GW

- Distributed PV: remains the big unknown; considering that installations are likely to increase in H2 when prices are lower and considering the 2.4 GW installed in Q1, full-year installations of 9–12 GW are possible

- Apricum 2017 forecast: 37–42 GW

In summary, Apricum believes that the Chinese market is still overheated in 2017, fueled by momentum from an unsustainable pipeline of utility-scale projects that are unlikely to secure the rights to FiT funding in the near term. At the same time, the market is moving in a healthier direction with the rise in distributed PV reducing curtailment rates nationwide. With the diversification away from utility-scale FiT as the main driver of demand, component demand and prices are likely to become more even across the year, not just in China but also globally.

The gradual loss of domestic utility-scale FiT and subsequent margin squeeze is likely to push Chinese companies to seek market share overseas, which would have strong ramifications on small-scale midstream and downstream local players globally. Non-Chinese manufacturing players should watch carefully the developments in the Top Runner Program this year, as well as any updates to the minimum Top Runner criteria. These to some extent serve as a technology development roadmap for the Tier-1 Chinese companies – more on this in an upcoming article on the Top Runner program.

On the other hand, the cumulative 105 GW PV target under 13th Five Year Plan can be safely ignored; the key takeaway here should be the clear government intention to drive PV activity towards the distributed segment. A very large market is expected to remain for utility-scale as well, as the country is heavily incentivized to keep its enormous solar manufacturing sector utilized.

Notes

Please note that the terms “PV Poverty Alleviation Program”, “PV Build Plan” and “Renewable Subsidy Catalog” are Apricum’s independent translations of the Chinese-language equivalent, as there are as yet no widely-used English names.