The MENA region is starting to witness a drastic increase in large-scale battery energy storage systems (“BESS”) projects, accompanying a soaring penetration of renewable energy. This has happened at a pace, which seems to have surprised many market analysts.

In the past, forecasts for the MENA region showed a few GWh for the coming years at best. Usually, the region was not even split into individual countries, but combined into a broad “other” bucket

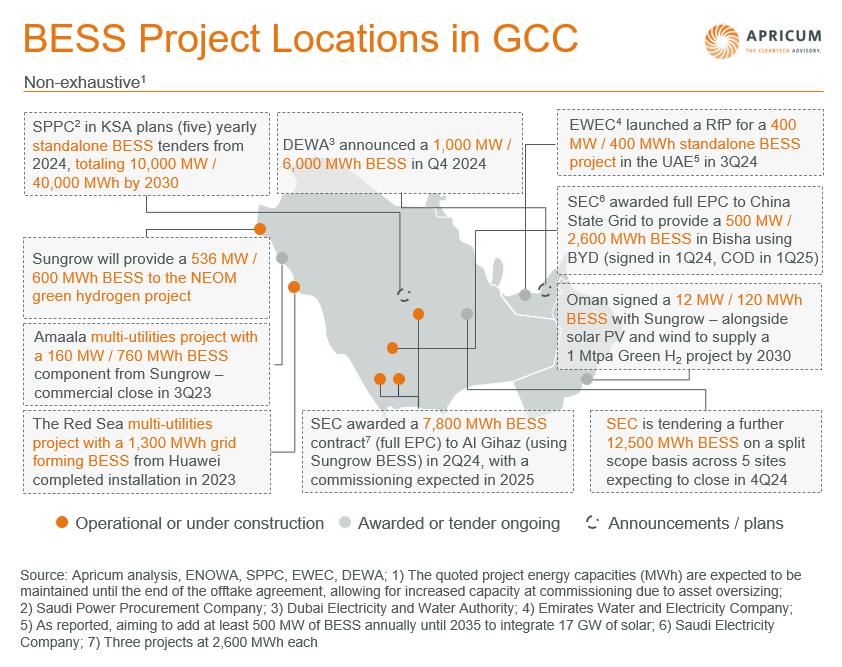

However, if you add up the numbers for Saudi Arabia (KSA) alone, we end up at 13 GWh of grid-scale BESS operational or in construction already today. And if we add recent tenders, this will lead to a whopping 33.5 GWh of BESS capacity by 2026. This would make Saudi the third biggest global BESS market after the USA and China.

While KSA is certainly leading the pack, increasing deployments can be witnessed all across MENA and the Gulf or GCC region in particular. The main drivers have been the launch of industrial green hydrogen and multi-utility projects for giant tourist resorts featuring solar PV and wind generation within large-scale microgrids. But more importantly, deployments are being driven by the material increase of intermittent renewable energy resources (RES) fueled by ambitious decarbonization targets and the need to support their integration into the grid.

BESS for integrated projects and large-scale microgrids

Oman (with its target production of 1 Mtpa of green hydrogen by 2030), the UAE (with its target production of 1.4 Mtpa of low-carbon hydrogen by 2031) and Saudi Arabia (via NEOM) are each launching several green hydrogen initiatives, where large-scale, fully integrated projects will include sizeable BESS components. The NEOM Green Hydrogen project, which aims to be powered by 100% renewables, is under construction and is already deploying a BESS 536 MW / 600 MWh facility supplied by Sungrow.

Saudi Arabia is also developing several landmark tourist complexes, where multi-utility contracts encompassing wind, PV, water, and BESS are awarded under single contracts to private utilities. For example, ACWA will deploy a 1,300 GWh BESS unit under the Red Sea multi-utility project and EDF a 160 MW / 760 MWh BESS unit under the Amaala project.

BESS for integration of renewable energy in GCC grids

The UAE and KSA governments have set ambitious targets for the share of clean energy in the electricity mix, e.g., 50% renewable energy and 50% natural gas by 2030 in KSA. The UAE and Saudi Arabia have already deployed 9 GW and aim to reach 144 GW of renewable power capacity by 2030. Large-scale power plants recently connected to the grid enjoy incredibly low LCOEs below 2 USD cents.

The universal benefits of BESS apply just as strongly to the MENA region: they can support in harnessing the full potential of renewable energy by storing & shifting record low-cost PV or wind power generation to times of the day when demand for electricity is at its highest. In addition, BESS can provide operational reserve and ancillary services such as frequency response, voltage regulation and black start, replacing part load operation of existing power plants and reducing pressure on the grid.

Most of the projects are expected to be procured by government-owned public entities, such as SPPC, SEC, EWEC and ENOWA (NEOM).

The Saudi Electricity Company (SEC) awarded a 7.8 GWh BESS contract to Al Gihaz (using a Sungrow BESS) in Q2 2024 with commissioning expected in 2025. Furthermore, SEC is tendering a 12.5 GWh BESS on a split scope basis across five sites in KSA expecting to close in the fourth quarter of 2024.

The Saudi Power Procurement Authority (SPPC) is planning annual standalone BESS tenders of 2 GW / 8 GWh from 2024 onwards, totalling 10 GW / 40 GWh by 2030. In the UAE, Emirates Water and Electricity Company (EWEC) issued in July 2024 a RfP for a 400 MW / 400 MWh standalone BESS project.

These offtakers conduct BESS procurement either through the EPC route, where they procure the BESS product, or via the IFP route, where they procure flexibility services. The latter is expected to dominate in the future with an availability-based payment structure covering all use cases.

IFP deployment and related risks

IFP (Independent Flexibility Provider, the storage equivalent to an Independent Power Producer or IPP) projects will follow a PPP (Private-Public Partnership) framework, relying on project finance. Procurement-related agreements must ensure well-structured risk allocation among stakeholders and effectively mitigate key risks to facilitate capital raising from lenders, such as commercial banks and equity developers, who may be unfamiliar with this pioneering project type in the region.

Key risks to be considered from the bankability standpoint in IFP projects include operational uncertainties and the risk of technological failure.

To mitigate operational uncertainties and their impact on the asset’s economic life, the offtake agreement must clearly define the operation / dispatch regime (e.g., number of discharge cycles per day) and compensate for incremental costs caused by any accelerated degradation if this operating regime threshold is exceeded. As such, utilization and degradation risks are covered by the offtaker, while other technical management risks are covered by the project owner.

To manage risks related to technological failure of the BESS, Tier-1 BESS suppliers can provide product warranties for the entirety of the offtake duration, typically 10–15 years, provided the warranty documentation is back-to-back with the operational parameters outlined in the offtake agreement.

In conclusion, the MENA region, led by the GCC, is emerging as a significant market for BESS. As public entities drive BESS procurement and the IFP route is expected to dominate the market, well-structured risk allocation and mitigation strategies will be crucial to ensure bankability and capture the opportunity.

How Apricum can help?

With nearly a decade of experience in project finance and a dedicated focus on energy storage, Apricum has access to C-level executives of developers for effective consortia formation. We understand lenders’ funding appetites and developers’ bid optimization strategies, enhancing project competitiveness. Additionally, as financial advisors, Apricum can leverage our global contacts with BESS integrators to address key pain points and streamline execution. Contact Managing Partner Nikolai Dobrott for further information.

This article was written by former staff members Corentin de Ricaud and Daria Kuzmina.