Germany’s Secondary Control Reserve (SCR) market has attracted significant interest from many energy storage players in the past. Requiring minimum energy capacities of at least four hours and energy delivery for even longer periods, the SCR market particularly appealed to players with long-duration energy storage solutions, such as redox-flow batteries, as well as aggregators of small residential systems looking for additional revenue streams. Although these players closely examined the SCR market opportunity and its economic viability, decreasing prices along with the need for a rather complex bidding strategy have prevented the SCR market from following a similar path to that of the Primary Control Reserve market, which already has more than 140 MW of battery capacity installed.

On June 13, 2017, Germany’s Federal Network Agency (or Bundesnetzagentur) published some long awaited updates to the Secondary and Minute Control Reserve (MCR) markets’ tendering conditions and publication requirements, concluding a one-and-a-half-year-long process. The primary objective of these updates is to provide better access for renewable energy generation, flexible demand and storage assets to Germany’s ancillary services markets.

In this article, my colleague Stephanie Adam and I take a closer look at these new SCR tendering conditions and publication requirements and assess their implications for energy storage.

Key changes in SCR tendering conditions

Five key changes will come into force a year from now, in July 2018.

1. Auction frequency increases, delivery periods are shortened:

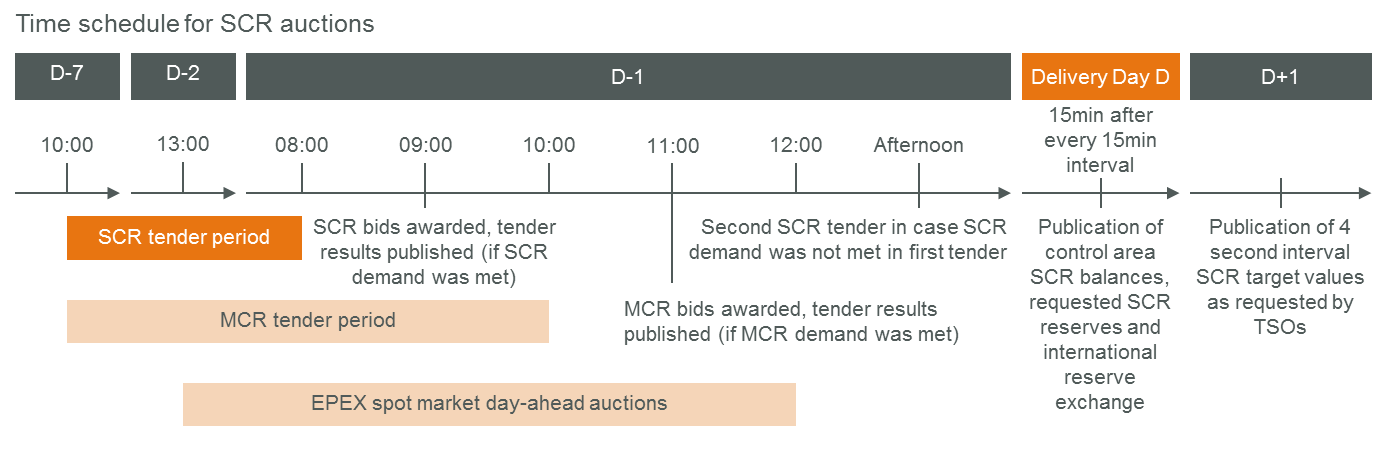

SCR auctions will take place daily instead of weekly and delivery periods will be shortened from one week to one day; auctions will open one week ahead of the delivery day at 10:00 am and close at 08:00 am the day before delivery.

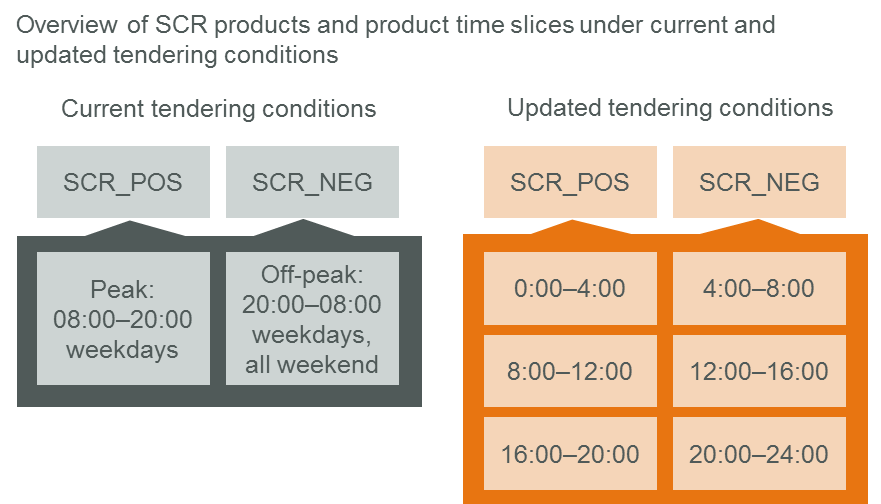

2. Product time slices are shortened:

There are two SCR products: 1) Positive SCR or SCR_POS and 2) negative SCR or SCR_NEG. Both products are currently auctioned in two distinct product time slices, peak and off-peak. The new SCR tendering conditions foresee more but shorter product time slices: There will be six product time slices[1] for each SCR product with a duration of four hours each.

Source: Apricum

3. Bids <5 MW can be admitted:

Minimum SCR bid size is currently 5 MW and this will remain the regular required minimum bid size. However, offers of 1 MW, 2 MW, 3 MW or 4 MW can be admissible in the future if the bidder submits only one bid per SCR product, time slice and control area[2]

4. Asset collateralization facilitated:

Asset pooling remains permissible only within a given control area but reserve collateralization (needed to secure reserve provision in case of failure of a technical unit) can now occur with prequalified assets from other control areas

5. Data transparency increases:

Four second interval data on SCR target values sent from the TSOs to the connected SCR providing technical units will be publicly available on the day after delivery

Implications for energy storage

The outlined changes impact energy storage participation in the SCR market in various ways.

More efficient interaction between SCR, MCR and day-ahead spot market

The updated tendering time schedule enables closer interaction between the SCR, minute reserve and spot market, resulting – most likely – in more efficient pricing. SCR auction results will be available within an hour after auction closure, by 09:00 am on the day before delivery. This is just in time to allow participation in the minute reserve market (auctions close at 10:00 am) or in the day-ahead EPEX spot market (auctions for Germany and Austria are open until 12:00 pm). This means that alternative revenue streams can be accessed in case of an unsuccessful SCR bid. A better alignment of SCR, MCR and day-ahead auctions will also make the opportunity cost of SCR market participation more transparent. Currently, SCR is tendered every Wednesday, the one-week-long delivery period starts in the following week. At the point of bid, transparency on power generation and demand in the following week is limited. Once set, the terms of SCR supply cannot be modified. Therefore, it is currently impossible to adequately consider short-term signals from the day-ahead spot market in SCR pricing decisions. In the future, bidders who anticipate price spikes in the day-ahead market may decide to withhold their SCR bids and deliver to the spot market instead.

Source: Bundesnetzagentur

Minimum required energy capacity limited to 4h at most, reducing capex

Shorter product time slices will reduce minimum storage capacity requirements. Prior to the regulatory update, network operators indicated that full capacity provision over four hours would be the required minimum storage capacity[3]. However, since SCR capacity is often demanded continuously for more than four hours, prequalified providers were required to guarantee energy delivery for even longer periods. With the reduced, four hour product time slices, this will no longer be required and four hour storage capacity will definitely be sufficient. As prequalification requirements evolve, network operators might even decide to accept smaller energy storage capacities if the asset owner demonstrates a reliable charging strategy.

More efficient utilization of pooled storage capacities, boosting revenue potential

Specifically for aggregators who “pool” multiple behind-the-meter storage units, daily auctions and shorter product time slices allow for more targeted marketing of available storage capacities. Instead of limiting offers to the minimum available pool capacity within a week’s relevant 12-hour time slice, bids can now be flexibly tailored to prosumer load profiles (in four hour increments). For example, bids can reflect that home storage assets are typically charged with PV power during the day, discharge energy in the evening or early morning and are often not used at night. Differences between weekday and weekend consumption can also be considered. A given storage pool will thus be able to sell more capacity into the SCR market than currently. Furthermore, admissibility of bids <5 MW grants smaller pools access to the SCR market. This lowers the aggregation threshold for storage companies that plan to tap the SCR market for additional revenue streams.

Easier to secure reserve availability, a win for smaller players

Admissibility of asset collateralization across all control areas makes it easier to secure reserve availability throughout the delivery period. Especially small players struggled in the past to find a suitable counterparty to collateralize their SCR capacity within a given control area. These players can now either use their own assets located in other control areas as collateral or access a larger pool of possible counterparties.

Better data availability, increasing market transparency

Market transparency will definitely increase. Currently, four second interval data is only available on SCR demand (not target values sent by TSOs) and can only be accessed by current or potential market players upon request. Energy payments to SCR providers, however, are based on target values for SCR delivery[4], not SCR demand and – according to the Bundesnetzagentur – both variables can differ substantially. Publication of four second time interval data on SCR target values will provide unrestricted access to the data that is needed to judge SCR market attractiveness and derive bid strategies.

Conclusion

While the described updates in tendering conditions and publication requirements for Germany’s SCR market are a definite improvement in market conditions for energy storage players, we still consider the SCR market a very challenging field for battery energy storage.

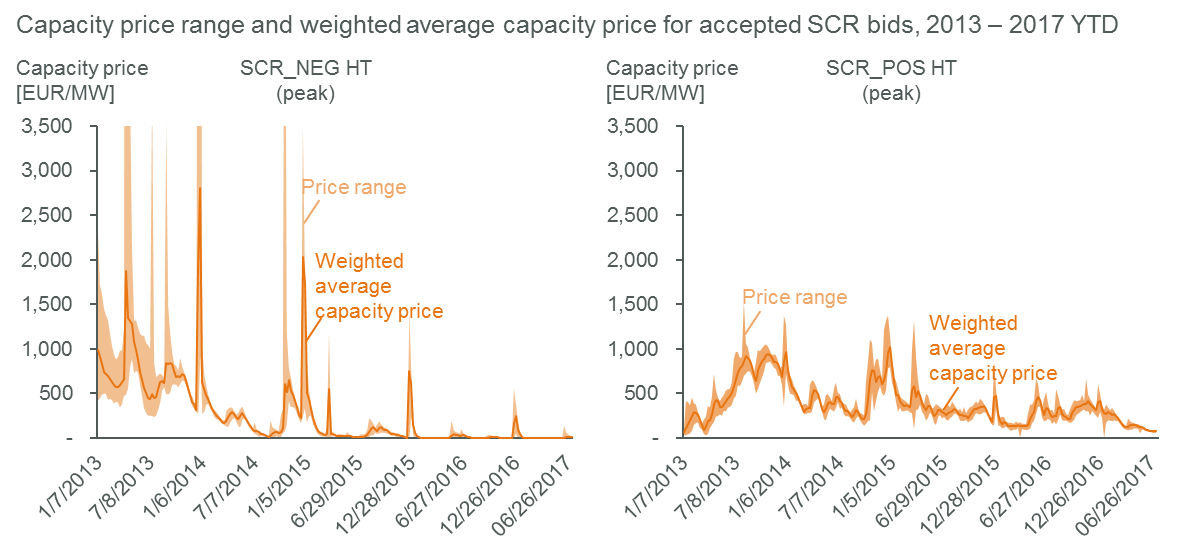

At current price levels and reserve activation frequencies, economic viability of SCR as a stand-alone use case is still hard to achieve. The aforementioned updates will likely intensify competition in a market with constant demand and thereby lead to further price declines.

Source: Regelleistung.net

Furthermore, SCR remains a merchant market with uncertain and volatile cash flows and thus hampers bankability. On any given day, it is never certain how much money – if at all – a storage asset can and will generate.

All in all, we do not expect the updated SCR tendering conditions to open up a big new stand-alone opportunity for energy storage in Germany. To what extent SCR can serve as an add-on to one or more other use cases, however, depends on the specific business model and must be assessed individually.

To learn more about the developments, challenges and opportunities in the German energy storage market, consider subscribing to Apricum’s Energy Storage Briefing, a biannual report providing comprehensive analyses with focus on the two major energy storage markets in Europe – the UK and Germany. Please contact Florian Mayr for further information.

[1] 0:00 to 4:00; 4:00 to 8:00; 8:00 to 12:00; 12:00 to 16:00; 16:00 to 20:00; 20:00 to 24:00

[2] Defined by ENTSO-E as a coherent part of the interconnected system operated by a single system operator.

[3] “Would be” since there is currently no operational stand-alone storage asset with primary use-case SCR in Germany

[4] Or actual SCR delivery values