If you ask a random person on the street what a battery is used for, they would probably first think of the useful items keeping their laptops, smartphones and (electric) cars working. In fact, mobile devices account for the most widespread usage of batteries these days (about 85% of the market volume in 2014). Recently however, the number of battery energy storage systems (BESS) used for stationary applications, both utility-scale and distributed, has started to grow significantly. According to recent estimates, today’s annual market volume of about USD 1B is expected to reach an impressive USD 20–25B by 2024 – hence, it is worth having a closer look at what is driving this market.

Three major drivers of growth for stationary BESS

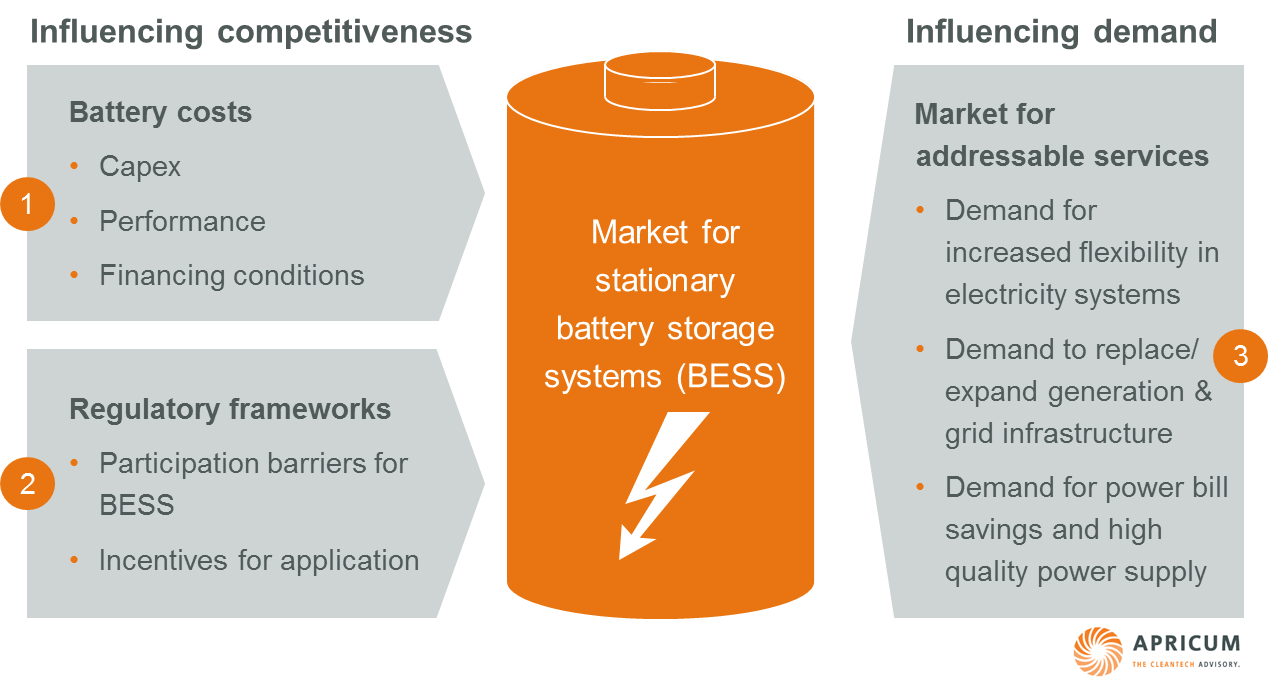

Simply explained, the growth of stationary BESS is driven by positive developments in 1) battery costs and 2) regulatory frameworks that both increase the competitiveness of batteries to participate in 3) a growing market for addressable services.[1]A fourth growth driver is the more suited application of BESS in specific settings, e.g., increased energy density to meet space constraints or improved safety by using non-toxic, non-flammable materials. However, due to the relatively lower impact on stationary applications, this aspect is not covered in more detail in this article

- Battery costs

The key prerequisite for the widespread application of stationary BESS is a decrease in the related costs over the lifetime of the battery. This can be mainly achieved through reduced capex, performance improvements or better financing conditions.

- Capex:

The BESS technology that has seen the biggest cost decline in recent years is lithium-ion (Li-ion), which has dropped from about 500–600 USD/kWh for an automotive battery pack in 2012 to about 300–500 USD/kWh[2]Prices for MW-scale systems range between 500–700 USD/kWh in 2015 in just three years. This was mainly driven by the technology’s dominant position in mobile applications such as “3C” (computer, communications, consumer electronics) and e-vehicles and the resulting economies of scale in manufacturing. In this context, Tesla is aiming to further drive down costs of Li-ion through its planned 35 GWh/a “Giga-Factory” in Nevada. Newcomer Alevo has announced similar plans by transforming an abandoned cigarette factory into a 16 GWh/a battery manufacturing site.A different approach to low capex is pursued by most energy storage technology startups today. Being aware that they will have a hard time catching up with the production volumes of established technologies such as Li-ion, companies like Eos, Aquion or Ambri are designing their batteries to meet a certain cost point right from the start. This can be achieved by pursuing a cell chemistry that allows using abundant and cheap raw materials for electrodes, membranes and electrolytes, as well as allowing for a high automatization and outsourcing of production to global scalable manufacturing contractors such as Foxconn. As a result, Eos for example is claiming a price point of only 160 USD/kWh for its MW-scale system. Also, innovative sourcing can help to reduce investment costs for stationary BESS. For example, Bosch, BMW and Swedish utility Vattenfall are installing a 2 MW/2 MWh stationary storage system based on used Li-ion batteries from BMW i3 and ActiveE cars.

- Performance:

Performance parameters can be improved both at a manufacturing and operational level to lower the lifetime cost of BESS. The lifetime of the battery (both calendar and cycle life) obviously has a strong impact on the battery’s economics. At a manufacturing level, increases in lifetime can be achieved by adding proprietary additives to the active chemicals as well as by improvements in the production process to reach a more homogenous cell quality. The degradation of the battery’s capacity over time can be diminished, for example, by adding mechanical elements to lead acid batteries in order to prevent dendrite formation. Although obvious, the battery should always work efficiently within its designed operating limits, for example, when it comes to the depth-of-discharge (DOD). By restricting the possible DOD in the application or by using systems with a capacity higher than required can dramatically increase the cycle life. Detailed knowledge about the optimal operating limits, obtained through rigorous lab testing, and having a proper Battery Management System (BMS) in place, is a big advantage.Round-trip efficiency losses are mainly due to the hysteresis inherent in the individual cell chemistry. However, applying an adequate rate of charging or discharging and, again, DOD helps to maintain high efficiency. Also, the energy consumed by components of the battery system, i.e., cooling, heating or the BMS, impact the efficiency and should be kept to a minimum.

- Financing conditions:

The bankability of stationary BESS projects is often affected by a limited track record and a general lack of experience of financing institutions regarding performance, maintenance and business models in the battery storage segment. Vendors and developers of BESS projects should try to improve the investment conditions, e.g., by standardizing warranty diligence, by structuring deals towards front loaded returns or by implementing thorough testing processes for the battery.In general, with the aforementioned falling capex and an increasing number of batteries operating at a continuously high performance, investor confidence will increase and financing costs will fall.

2. Regulatory frameworks

Like all relatively nascent technologies entering an established market, BESS depend on favorable regulatory frameworks to a certain extent. At the minimum, this means the absence of participation barriers for BESS. Ideally, authorities will see the value in stationary storage and incentivize its application accordingly.

- An example of the impact of removing barriers is Order 755 by the US Federal Energy Regulatory Commission (FERC), which asks ISOs[3]Independent System Operator and RTOs[4]Regional Transmission Organization to provide performance payments for faster, more accurate and higher MW-mileage[5]Sum of absolute values of changes in output resources. Since independent operator PJM revamped its wholesale electricity market in October 2012 accordingly, energy storage has been on the rise, with the result that two-thirds of the 62 MW of storage deployed in the USA in 2014 was located in PJM’s territory

- In Germany, homeowners who want to purchase a PV-storage system can obtain a low-interest loan from the KfW, a German government-owned development bank, plus a cash grant of up to 30 percent on the purchase price. This has triggered the installation of about 12,000 systems to date, although it should be noted that another 13,000 systems were built outside the program

- In 2013 California’s regulator (CPUC) introduced the requirement that the state utilities must purchase 1.325 GW of storage capacity by 2020. This procurement program aims to demonstrate how batteries can modernize the electric grid and help the integration of solar and wind power

The examples mentioned above are all major events attracting significant attention in the energy storage world. However, also smaller, often unnoticed changes in regulations can have a powerful impact on the regional applicability of BESS. Potential examples include:

- By simply reducing the minimum capacity requirements for the German primary reserve market, owners of residential storage would be allowed to participate as virtual power plants, further strengthening the business case for distributed BESS

- Also in Germany, the recently published white paper for the new energy market design indicates higher prices for balancing group deviations, which could make battery storage very attractive for balancing group managers

- A core element of the EU’s Third Energy Package, which came into force in 2009, is the unbundling of companies’ generation and sales operations from their transmission network. In this context and due to some legal uncertainties, it is not entirely clear under which conditions a TSO would be allowed to operate an energy storage system. Improvements in legislation would set the ground for a wider application of BESS for grid support

3. Market for addressable services

Specific trends in global electricity markets are triggering a growing demand for services that can, in principle, be served by stationary BESS. Relevant trends are:

- The increasing need for flexibility in the electricity systems due to reasons such as the fluctuating nature of renewable energy and the urge to increase the resilience of power supply during natural disasters.[6]When hurricane Sandy hit the US east coast in 2012, more than eight million people were temporarily without electricity due to the destruction of (centralized) infrastructure Here, energy storage can provide ancillary services for frequency and voltage control, grid-congestion relief, renewable energy firming and black start capabilities among others

- The extension and reinforcement of generation and transmission & distribution infrastructure, caused by ageing or insufficient capacities and the increasing electrification of rural areas.[7]In case extension of grid infrastructure is driven by flexibility needs, this would be part of the previous trend In this context, BESS can be applied as an alternative to defer or avoid infrastructure investments, to stabilize island grids or improve the efficiency of diesel gensets in off-grid systems

- Industrial, commercial and residential end users are struggling with higher power bills in particular caused by time-of-day prices and demand charges. For (potential) rooftop PV owners, falling feed-in tariffs impact economic viability. Furthermore, electricity provision is often unreliable and of poor quality. Stationary batteries can help to increase self-consumption, perform “peak-shaving” and “peak-shifting” along with offering an uninterruptible power supply (UPS)

Obviously, there are various conventional, non-energy storage options for meeting this demand. Whether batteries constitute a better alternative must be assessed on a case-by-case basis and can vary strongly among geographies. For example, while there is a positive business case for T&D deferral in places like Australia or Texas with vast distances to overcome, the typical cable length at the medium-voltage level in Germany is less than 10 km, which makes a conventional grid extension the cheaper alternative in most cases.

Often, providing just one service with BESS is not sufficiently profitable. Hence, services should be combined to “benefit stacks” to allow for cost reductions and compensation through multiple mechanisms. Starting with the application with the largest revenue stream, spare capacity should first be used to seize on-site opportunities and avoid regulatory barriers, such as UPS. For any remaining capacity, services delivered to the grid, such as frequency regulation, can be considered as well. Needless to say the additional services must not get in the way of the primary service.

Implications for storage market players

Improvements within the drivers described above will bring about new business opportunities and the consequent growth of the market. However, negative developments can in turn lead to business models not reaching – or even losing – economic viability. For example, projected cost declines might not materialize due to unexpected shortages in a certain raw material, or the commercialization of new technologies is not progressing as anticipated. Changes in regulations could create a framework BESS cannot compete in. Also, developments in neighboring industries could create additional competition for stationary BESS, e.g., the use of (curtailed) renewable energy sources for frequency control: In some markets, such as Ireland, the grid code already requires wind parks to act as a primary reserve.

Consequently, it is vital for companies to closely follow, anticipate and even actively influence the developments in battery costs, regulatory frameworks and demand to successfully participate in the global market for stationary battery storage.

Apricum supports the growth of BESS market players including manufacturers, developers, users (e.g., utilities, TSOs) as well as investors. Our service range includes transaction advisory such as sell-side and buy-side mandates along with strategy consulting for identifying and seizing the most attractive business opportunities around the world.

For questions or comments, please contact Principal Florian Mayr, head of Apricum’s hybrid, energy storage and wind practices.

[1] A fourth growth driver is the more suited application of BESS in specific settings, e.g., increased energy density to meet space constraints or improved safety by using non-toxic, non-flammable materials. However, due to the relatively lower impact on stationary applications, this aspect is not covered in more detail in this article

[2] Prices for MW-scale systems range between 500–700 USD/kWh in 2015

[3] Independent System Operator

[4] Regional Transmission Organization

[5] Sum of absolute values of changes in output

[6] When hurricane Sandy hit the US east coast in 2012, more than eight million people were temporarily without electricity due to the destruction of (centralized) infrastructure

[7] In case extension of grid infrastructure is driven by flexibility needs, this would be part of the previous trend