The stationary energy storage market is a complex animal.

Probably only few other markets are based on a product as versatile and as suitable for a multitude of applications, with equally dynamic costs and pricing developments and the same level of dependence on individual national regulations.

As a result, the market is characterized by a landscape of heterogeneous “pockets of opportunities”, a concept that is key to understand for being successful in energy storage.

What is a pocket of opportunity?

Energy storage market growth requires three prerequisites:

1. Competitiveness of energy storage to provide a certain service

2. General demand for this service

3. Suitable regulatory and market frameworks

For the sake of simplicity, let’s combine prerequisites 2 and 3 and call it “addressable demand”, i.e., demand that can be accessed and monetized through energy storage.

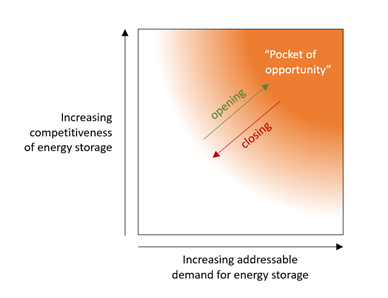

A pocket of opportunity occurs between those two dimensions: Competitiveness and addressable demand (see figure below). As both are typically tied to the specific challenges, rules and competing solutions of an individual power market, it usually makes sense to confine a pocket of opportunity to within the same (geographic) boundaries.

How a pocket of opportunity opens

A pocket of opportunity opens if energy storage starts to competitively serve a use case with a minimum level of addressable demand.

For example, when

- the value of a use case increases (e.g., increasing power price spreads in UK sufficiently covering storage costs and allowing for arbitrage),

- the need for flexibility grows (e.g., variable renewable energy shares in the generation mix reaching substantial level),

- regulatory barriers for energy storage are removed (e.g., USA’s FERC rules requiring access for storage to wholesale markets),

- and/or new market schemes are established (e.g., “grid booster” scheme in Germany allowing storage to get paid for mitigating grid congestions)

With growing or at least constantly high demand and continued competitiveness, the pocket of opportunity remains open and can even expand.

How a pocket of opportunity closes

As quickly as a pocket of opportunity can open, it can close as rapidly again.

Typical reasons observed in the market are:

- Most prominently, supply for a service exceeding demand (e.g., German market for Primary Control Reserve being increasingly saturated)

- The abolishment of market schemes (e.g., UK’s temporary ODFM service being wound down as the impact of the first pandemic lockdown vanishes)

- A change in regulations to the disadvantage of storage (e.g., de-rating introduced for UK’s capacity markets resulting in significant revenue cuts for storage)

In particular, the latter can cause a pocket shutting down at a rapid pace, in the worst case turning a profitable storage unit into a stranded asset in no time.

So what?

But how to successfully navigate the energy storage markets and their oscillating pockets of opportunities?

One prerequisite is to remain flexible enough to swiftly leave closing pockets and seize opening ones. To give a few examples, whenever possible, do not lock in on a specific use case/a specific mode of operation of the storage unit. Also, try to keep a technology-agnostic approach. Accommodate remote software updates and ensure easy modifications of your hardware. Furthermore, negotiate flexible warranties.

Another probably obvious one is to influence the two dimensions spanning the pocket of opportunity: While addressable demand is hard to control apart from lobbying work, competitiveness of storage is something that can be actively engaged in. The storage offering must be continuously improved according to cost, safety and other success factors. Don’t be forced to leave a pocket of opportunity while it’s still open for others.

Last but not least, maintain an up-to-date understanding of the biggest, most attractive pockets of opportunities around. Once addressed, they will feed you and your business for a very long time. In a recent article, I identified “renewables-plus-storage” and “stacking of merchant opportunities” as the main utility-scale drivers of the commencing decade of energy storage. Both applications directly tap into the vast global demand for electricity itself – which represents the deepest pockets of opportunity energy storage has to offer.

For questions or comments, please contact Apricum Partner Florian Mayr.