In the second of a two-part series on opportunities in battery energy storage in Europe, Apricum Partner Florian Mayr and Senior Consultant Dr. Hendrik Kienert discuss the key drivers, challenges and outlook for today’s main use cases in the UK and Italy. Together with Germany, which was the focus of part one of this article, the UK and Italy are the most relevant markets in Europe with respect to capacities installed and planned pipeline.

Progress in the UK: Call for Evidence, Enhanced Frequency Response and Benefit Stacking

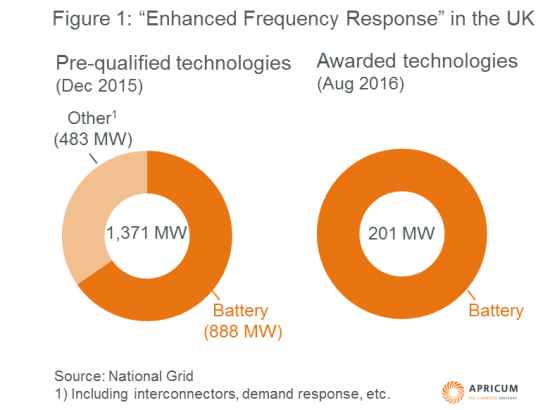

The UK battery energy storage market is currently making significant progress. A long awaited “Call for Evidence” by the Department for Business, Energy and Industrial Strategy (BEIS) was published in November 2016 with the aim, among others, to define a clear regulatory framework for storage. This framework has to address issues like operating licenses and double payments of fees for charging and discharging due to the grid code. Also, the first tender of the newly introduced enhanced frequency regulation (EFR) service was completed in August 2016. While there are multiple use cases for energy storage in the UK, including several services sourced for grid stabilization, EFR provides the largest potential for battery energy storage systems (BESS) so far.

With the planned phase-out of coal power plants by 2025, potentially even by 2022, a future shortfall of inertia provided by conventional generators needs to be compensated for as it makes the system more susceptible to frequency changes due to an imbalance of supply and demand. Batteries can fully play off their strength in performing this task by counteracting supply-demand imbalances within the extremely short notification period of less than one second, which is required by the EFR scheme and which does not allow fossil-fuel technologies to compete. This is a key difference to other grid-stability services such as Firm Frequency Response (FFR), Fast Reserve (FR) and Short-Term Operating Reserve (STOR). So it is not surprising that the majority of pre-qualified projects were based on batteries and that the complete tender capacity of 200 MW was finally awarded to battery bids, as illustrated below in Figure 1.

Service providers are compensated based on a pay-as-bid basis and the high level of competition in the bidding process has resulted in a low average winning price of ~GBP 80k per MW per year. However, the contract period of four years gives considerable planning security and is a step towards enabling project financing, though it is most likely not sufficient to fully amortize the asset.

In addition to pure frequency control, there seems to be a serious attempt by the regulator and distribution network operators (DNOs) to enable benefit stacking, thereby improving the economic viability of energy storage. This can be seen from pilot projects assessing the opportunities of combining several revenue streams, both in front and behind the meter as well as from the flexibility provided by the National Grid to the EFR tender participants who were free to choose specific time windows for addressing additional use cases with their BESS. For instance, EFR projects were already awarded in the recent capacity market auction for Q4 2020/Q1 2021, which makes the full amortization of the battery more feasible.

Opportunities for Distributed Energy Storage

Additionally, different current and future applications of distributed energy storage exist in the UK – for residential as well as for commercial customers.

Increasing Residential PV Self-Consumption

Residential storage is often highlighted as a big opportunity in Britain, which is mainly explained by the high number of households with rooftop PV and a decreasing feed-in-tariff (FiT).

However, two components of the UK FiT have to be distinguished: the generation tariff paid for every kWh generated and the export tariff paid for each kWh sent to the grid. The generation tariff has indeed been substantially reduced recently and leads to lower attractiveness of residential PV in general, but the impact of this cannot be mitigated by adding a storage system. In contrast, the export tariff has been slightly increased and is not expected to be reduced in the coming years. But only a reduction of this export tariff would make grid feed-in less attractive and therefore PV self-consumption and energy storage more attractive.

Hence, compared to Germany, the current FiT in combination with lower retail prices for electricity at 22 EURct/kWh (in 2015), less irradiation and the lack of an incentive program make PV self-consumption a more difficult business case for storage in the UK. Still, early movers’ interest in energy self-sufficiency is a significant driver for residential battery storage, attracting domestic and foreign residential storage companies to enter the market, e.g., Solarwatt with the launch of its MyReserve system in Q1 2017.

Additional economic benefits, however, can be realized by aggregating residential batteries to provide grid-services to utilities or to participate in energy trading. Different types of such models are currently being explored by several players in Europe and have the potential to make residential storage more viable. In the UK, local player Moixa offers its “GridShare” option and aggregates storage systems to take part in grid services, especially via the FFR scheme. Customers are typically rewarded either via a fixed annual payment or a share of the overall revenue generated.

Benefitting From Time-of-Use Pricing

Another potential revenue source of distributed storage systems is based on time-of-use pricing: Charging the battery at times when electricity rates are low and discharging during peak price periods. In the UK, such time-of-use tariffs are already available (“Economy 7” and “Economy 10” tariffs) and are likely to become more widely adopted in the future with the rollout of smart meters, which is planned for completion by 2020. These tariffs are designed based on 7 and 10 off-peak hours, respectively, predominantly during night time. Typically, they start to become financially attractive when at least ~40% of consumption occurs during off-peak hours, which is only the case in specific situations if no type of energy storage is applied.

Avoiding Network Fees

Larger commercial customers may further profit from reduced network fees that apply for the transmission network (TNUoS) as well as for the distribution network (DUoS). These fees consist of multiple components that partly depend on detailed usage patterns. In this context, energy storage systems allow the time-shifting of electricity consumption from the grid in ways that result in lower fees, i.e., by charging the batteries in time periods with normal or low demand and discharging the battery during peak demand.

Each year, the three 30-minute periods of the winter season with the highest overall power demand, the “triads”, are retrospectively determined. As the transmission network fees depend on a customer’s power consumption in these triads, there is an incentive to plan for overall lower power consumption during periods of likely peak demand.

Similar considerations apply to the distribution network fees. Here, the corresponding unit charge per kWh consumed depends on predefined time periods. This leads to an even simpler way of reducing charges by shifting grid consumption to lower cost periods.

Considering all aspects together, the UK energy storage market is becoming significantly more mature with opportunities arising from the EFR scheme and multiple other use cases that can be partly addressed with benefit stacking.

Key Energy Storage Use Cases in Italy: Terna’s Grid Development and Grid Defense Plans

In contrast to the UK, Italy does not exhibit such a massive pipeline of energy storage projects like the 200 MW tendered under the EFR scheme. However, when it comes to installations already operational, no European country except Germany has a higher capacity of utility-scale installations than Italy with its 56 MW.Back in 2010, Italy’s transmission system operator (TSO) Terna was facing two major problems caused by increased renewable energy generation in southern Italy. The first was significant grid congestion experienced on the mainland. The second was a reduction of inertia due to an increasing number of fossil power plants on the islands of Sicily and Sardinia running at limited load.

Consequently, Terna initiated two energy storage plans through open European tenders as illustrated in Figure 2. The first was the “grid development plan”, to relieve grid congestion with 35 MW of storage. Projects have already been completed entirely with NaS batteries from NGK. The second initiative was the “grid defense plan” for insular grids. The first phase, known as Storage Lab, has almost been competed with the installation of 16 MW of various energy storage technologies (lithium-ion, flow batteries, supercapacitors). The second phase of 24 MW is yet to be realized.

On the peninsular of Italy, flexibility options, such as interconnections to neighboring countries are limited. Furthermore, with more than 10% of the Italian population living in Sardinia and Sicily, the electricity supply on these islands remains an important issue for the national TSO. However, there are no official plans by Terna to extend the existing program beyond the remaining 24 MW. On the bright side, Terna invested significant money and time in understanding the applications for energy storage, at both the generation and retail level. It is therefore likely that these insights will trigger more energy storage projects in Italy.

Additional Use Cases in Italy

Although Terna is responsible for 90% of all existing and planned energy storage capacities at the moment, they are not the only ones pursuing activities in this sector.

Addressing Various Use Cases by Co-locating Storage with Renewable Energy Plants

Italy’s biggest utility, Enel, is testing the co-location of energy storage with both wind and solar in pilot projects in Sicily and on the mainland. Examples are a 2 MWh lithium-ion battery in conjunction with 18 MW of wind power in the province of Potenza and a 1 MWh nickel chloride battery together with 10 MW of PV power in Sicily. Given the grid constraints, there could be huge potential. Currently, it is already feasible to mitigate imbalances in PV generation, grid congestion relief and reduce penalties in the day-ahead and intraday markets, a specific feature in the Italian electricity market. Although business cases are not economically viable today, valuable insights gained together with continuous cost reductions and regulatory improvements are further advancing the case for energy storage.

Increasing Residential PV Self-Consumption

When it comes to residential storage, Italy offers high solar irradiation, one of the highest electricity rates in Europe and about half a million PV installed rooftop systems. However, larger-scale adoption of residential storage systems was delayed for quite some time because of regulatory barriers: Until April 2015, PV system owners were at risk of losing their right to incentives when installing battery storage. Now that this issue has been resolved and along with a tax deduction scheme subsidizing 50% of the costs in place, the Italian residential storage market is finally making significant progress.

Key market players such as Sonnen recognized the opportunities and began establishing distribution infrastructure in Q3 2015. At the moment, Sonnen has already around 25 sales centers in Italy, more than in any other country outside of Germany. And in November 2016, Italy became the first market after Germany, Austria and Switzerland in which Sonnen introduced its “sonnenCommunity”, a platform that aggregates residential energy storage systems in order to allow the “sharing” of stored electricity between participants. In March 2016, Tesla followed Sonnen and started serving the Italian market with its Tesla Powerwalls. After Sonnen sold about 400 systems in Q1 2016, the overall market – largely covered by Sonnen and Tesla – picked up speed with the result that more than 5,000 systems are expected to be sold by the end of 2016.

However, as in other European countries, the state of economic viability has not yet been reached and prosumers’ interest in energy self-sufficiency remains a key driver. Nevertheless, some economic benefit can be realized based on the spread between the electricity price and the remuneration for feeding PV-generated power into the grid. Almost all new residential PV systems are installed under the Scambio sul Posto (SSP) “net-metering” scheme. Typically, net-metering schemes allow for the later consumption of the same amount of energy that was fed into the grid earlier, therefore virtually acting as perfect “energy storage devices” and severely limiting the opportunities for residential batteries. In contrast, the Italian Scambio sul Posto scheme is more similar to a traditional FiT scheme and the compensation of the prosumer is based on the value – at the specific point of time – of the energy fed into the grid (a lower value at times of PV peak production) and additionally takes into account the costs of services (e.g., grid infrastructure). Therefore, the compensation for a kWh fed into the grid is not fixed and is complicated to predict. It usually amounts to around 12–14 EURct/kWh and should be viewed in the context of the household electricity price of approximately 25 EURct/kWh. This allows for a financial benefit per kWh charged and discharged slightly below the value seen in Germany.

Growing Opportunities for Energy Storage in Europe

In summary, the European market for energy storage, in particular in Germany, the UK and Italy, is set for continued growth, with more and more use cases becoming economically viable and regulatory barriers being removed slowly but steadily. Each market, however, features specific characteristics that determine the opportunities for energy storage. To successfully benefit from the growing market in Europe, a detailed understanding of each country’s needs, restrictions and developments is mandatory.

Apricum offers a range of services to accelerate entry into the European storage market. We offer support with raising funds from strategic and financial investors to finance expansion, conducting in-depth target market, use case viability and business potential analyses, and deriving the most suitable business development and partner company strategies.

For questions or comments, please contact Apricum Partner Florian Mayr.